Abstract

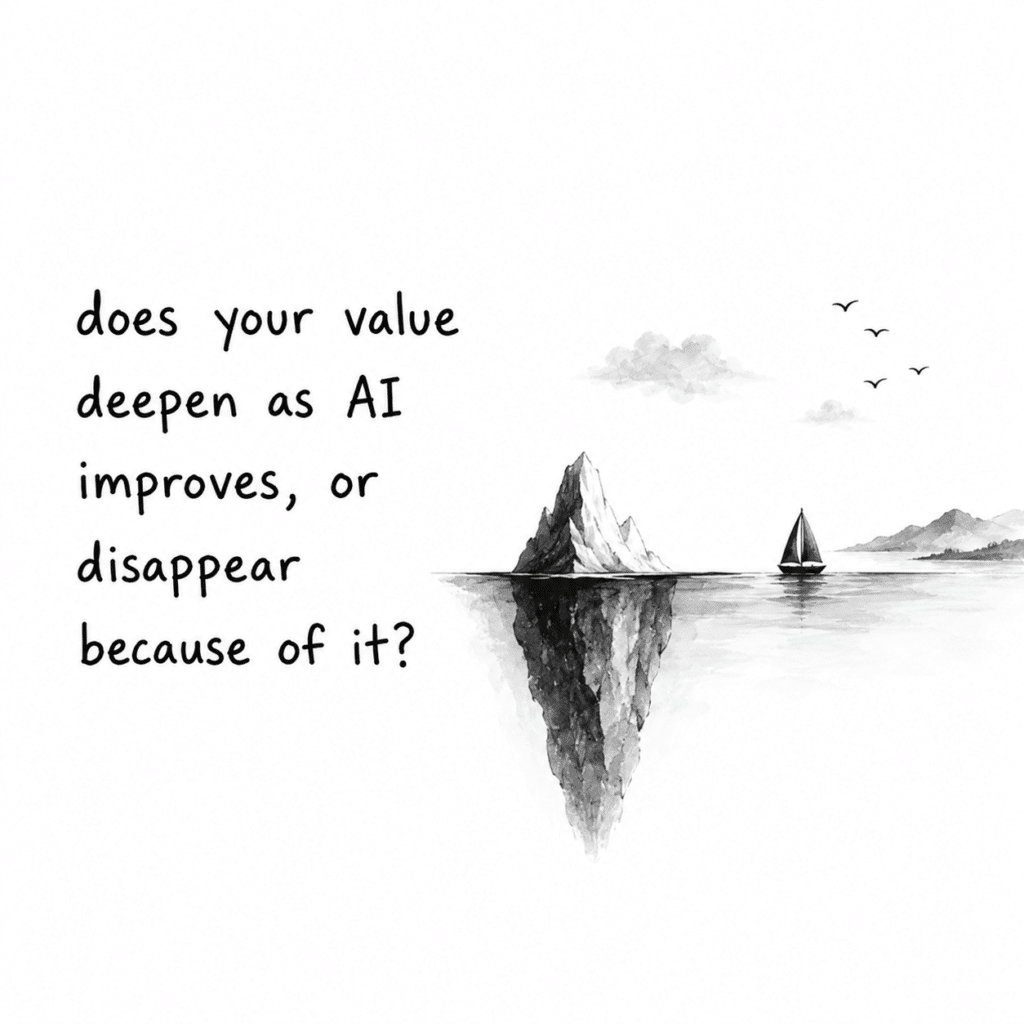

AI is making two types of business obsolete at the same time. Software startups that built products on top of AI providers are being absorbed — those same providers now ship the features directly. Established companies whose advantage was built on owning systems too complex for anyone else to touch are losing that advantage — AI makes those systems accessible to everyone. This article maps the five forces driving this restructuring — four that destroy value, and one that creates it. That fifth force is the paradox at the heart of the piece: the same technology doing the destroying is the one manufacturing new value, and it does both faster the more capable it gets. The diagnostic question that follows is not philosophical. It’s the most urgent thing a founder or executive needs to answer right now: does your value deepen as AI improves, or disappear because of it?

The Pattern That Will Keep Repeating

On Friday, January 30, 2026, Anthropic announced eleven specialised plugins for Claude Cowork — covering legal, finance, marketing, customer support, and other enterprise roles.[1] The legal plugin could review documents, flag risks, triage NDAs, and track compliance. Those are the tasks that form the revenue backbone of a multi-billion-dollar legal technology industry. When markets opened the following Tuesday, Thomson Reuters fell between 16% and 18%. Its largest drop in company history. RELX plunged approximately 14%. Wolters Kluwer dropped roughly 13%.[2] Within a week, the selloff had wiped nearly $1 trillion from global software and services stocks.[3]

Analysts called it the “SaaSpocalypse.” What it measured was market expectations, not demonstrated operating impact — and those are different things. Analysts at Artificial Lawyer put it plainly: the reaction was arguably irrational. Enterprise adoption takes time. The repricing ignored that.[4] But the direction of the signal isn’t in doubt: AI platform providers are no longer content to sell infrastructure — they’re absorbing the software businesses built on top of them, and they’ll do it again. If Anthropic can do this to legal tech, OpenAI can do it to customer support, Google can do it to analytics, and Microsoft can do it to productivity tools. That’s the part that should unsettle people.

It already has — twice, in the same month. On February 20, Anthropic launched Claude Code Security, a tool that reasons through source code the way a human security researcher would rather than matching against a database of known threat signatures.[5] The reaction swept across the security sector: CrowdStrike fell 8%, Cloudflare dropped 8.1%, Zscaler shed 5.5%. Claude Code Security specifically targets rule-based static code analysis — but the market initially treated all security vendors as equally exposed. Wedbush analysts argued the selloff was an overreaction — that AI-native security tools are more likely to become an additive layer than a replacement for established platforms.[6] That distinction, and that counterargument, deserve weight and are addressed in Section 5. Three days later, Claude Code’s COBOL modernisation capability sent IBM down 13% — its worst single session since 2000 — alongside Accenture and Cognizant.[7] Same mechanism. Three sectors. Twenty-four days.

What makes this moment distinct is that the pressure runs in two directions at once. Platforms are absorbing the high end of the application market. But the same platform that allows Anthropic to offer a legal compliance tool also allows a three-person accountancy firm to build its own compliance workflow — without writing a line of code. The market for off-the-shelf software tools is shrinking from both sides simultaneously — platforms absorbing it, end users reclaiming it.

This was market repricing based on expectations, not evidence of immediate displacement. When I first drafted this in March, I wrote that the real test would come in Q1 and Q2 2026 earnings — and that the numbers would prove more complicated than either the bulls or the panicked sellers expected. The Q1 results are now in. Here is the scorecard.[8]

What I got right. The panic overshot the near-term operating impact, exactly as the repricing-isn’t-displacement argument predicted. The “casualties” grew. IBM beat on revenue (+9.5%), with mainframe hardware up 51%. RELX’s legal division grew adjusted operating profit 12% — by selling its own AI tools. Thomson Reuters legal grew 9% organically on Westlaw and CoCounsel. Cybersecurity, treated as roadkill in February, recovered to records. None of these were displaced; several got stronger.

What surprised me. I underestimated how fast incumbents would convert AI from threat into revenue line — not in years, but in a single quarter. The structural exposure is real, but the direction of the first move was incumbents absorbing AI, not platforms absorbing incumbents.

What held. The pattern repeated on schedule: in May, Anthropic and OpenAI each stood up enterprise deployment arms within 72 hours, with Wall Street partnerships and open agent standards — the “they’ll do it again” claim, on time. And the structural pressure landed where the thesis said it would — not on legal research or behavioural security, but on documented, codifiable work: per-seat software (Salesforce roughly −30% year-to-date, Workday −33%) and the org chart itself (Section 6).

The restructuring is underway. The market repriced faster than operations moved — but the direction isn’t a guess anymore. The speed of displacement is lower than the panic implied; the certainty of it is higher than the relief suggests.

The Five Forces Restructuring the Economy

That single announcement didn’t appear in a vacuum. Over 70,000 AI companies have launched since 2022, and the failure wave is already well underway.[9] Five forces are driving it. Four share one root cause. The fifth is its mirror image — and the most important of the five.

AI can now execute documented, binary processes at very low marginal cost. Any workflow written down as a procedure. Any process codified as rules. Any logic expressed as if-this-then-that. AI can now execute all of it — without the human expertise that previously made it scarce. Startups that wrapped documented processes, incumbents whose premium was priced on documented complexity, cognitive labour that was rule-based and codifiable — all being repriced by the same underlying dynamic. This is a hypothesis about the mechanism, not a proven law; the following forces are the current evidence for it.

One clarification, because the whole argument turns on this one word. Codifiable means a competent practitioner could write the work down as a procedure complete enough for someone else to follow without independent judgment. It is not a synonym for “simple” or “low-value” — COBOL migration and legal document review are both highly skilled and highly codifiable. And it is a spectrum, not a switch: almost all real work is part procedure, part judgment. So the practical test is not “is my work codifiable?” but “where in my work does a human still have to decide something the instructions cannot specify?” That residue — the part that resists being written down — is your durable margin. Everything else is on loan from the platform. One caution, in the other direction: "tacit" is not a permanent safe harbour. Some of what looks like judgment today is simply work that hasn't been codified yet — the line keeps moving toward AI, so this is a test to re-run, not pass once.

The Wrapper Graveyard. Carta, a platform that tracks venture-backed companies, recorded 254 startup shutdowns in Q1 2024 alone — a 58% jump from the same period in 2023.[10] The pattern was consistent: startups built interfaces wrapped around GPT-4 or Claude’s API, charged $50–100 per month, and had no proprietary moat. Jasper AI entered 2023 with a $1.5 billion valuation generating marketing copy on OpenAI models.[11] As ChatGPT became widely available, Jasper’s revenue peaked at $120 million. Then fell to $35 million in 2024. Platform capabilities had outpaced it.[12] Chegg — an education platform whose core tutoring and homework product was built on a codifiable, rule-following process — has seen its stock decline approximately 99% from its 2021 peak as students shifted to AI alternatives.[13] Tome lost its edge when Microsoft integrated similar presentation capabilities into PowerPoint. Each of these products was a documented, rule-following process wrapped in an interface. At any moment, the platform they depend on can release an update that makes their entire product redundant. One update. Gone.

AI as a Deflationary Engine. AI is compressing the cost of cognitive labour — and this hits established advantages from two directions simultaneously. Time to market: what took a team six months can now be prototyped in a weekend. Resource requirements: a startup that needed $2 million to build a working product might now need $50,000. Those aren’t incremental improvements. They’re category changes. A lean challenger can reach product-market fit before a large organisation finishes its strategy review. That’s not competitive pressure. That’s a different game entirely. Figma’s rise illustrates this. It gained significant market share in design by moving faster with less. Adobe’s scale made that threat slow to recognise, and slower still to match.[14] On February 26, Jack Dorsey made the same logic explicit at Block. Gross profit was up 24%. The company was profitable. He still cut nearly 4,000 roles — almost half the workforce — citing AI replacing cognitive labour.[15] The stock surged approximately 20%. Bloomberg raised questions about whether the Block cuts represented genuine AI-driven efficiency or strategic cost reduction dressed in AI language.[16] The honest answer is probably both. Either way, the market rewarded the move.

Complexity Dissolution. IBM fell 13% on February 23 — not because a platform absorbed its features, but because Anthropic dissolved the premise of its value.[7] IBM’s COBOL moat was built on a 67-year-old language. That language powers an estimated $3 trillion in daily transactions. But underneath it all, COBOL code is documented binary logic. Every if-then statement is an explicit business rule written down in a programming language. When AI can read, map, and accelerate modernisation of that logic, the scarcity IBM was pricing comes under pressure. VentureBeat noted an important qualification: translating COBOL isn’t the same as modernising it.[17] IBM’s actual work involves system architecture, mainframe integration, regulatory compliance, and client relationships that go well beyond code conversion. The market’s $40 billion reaction may overstate the near-term threat. But it correctly identified something real: the easy part of what IBM charged for is now automatable.

The same pressure, qualified in the same way, hit Accenture, Cognizant, and India’s four largest IT firms, down 12–16% in nine sessions. It had already done the same to cybersecurity, three days earlier. Traditional SAST tools — static application security testing — work by matching code against a library of documented vulnerability signatures: if this pattern, then flag it. Documented binary logic. Claude Code Security doesn’t match against a rulebook; it reasons through code directly.[5] The market’s reaction was imprecise — it swept across the security sector, taking down CrowdStrike alongside SAST-adjacent vendors. But CrowdStrike’s Falcon platform uses behavioural AI and machine learning to detect threats, not signature matching, which is precisely why Wedbush called the reaction an overreaction for some of those names. The structural exposure sits with vendors whose actual moat was rule-based pattern matching: legacy SAST scanners, static vulnerability libraries, policy-based firewalls. The moat wasn’t expertise. It was a documented process that looked like expertise. The variable that determines exposure is not scale — it is codification. The more thoroughly a sector has documented its processes and codified its rules, the more thoroughly it has pre-written the instructions for its own replacement.

Capital Concentration and Dislocation. In 2025, AI startup funding reached approximately $202 billion — a 75% increase year-over-year.[18] Funding is highly concentrated: the two largest foundation model companies, OpenAI and Anthropic, captured 14% of all global venture investment between them. Fourteen percent. Between two companies. VCs are shifting their thesis from “does it use AI?” to “does it have a defensible position that AI platforms can’t absorb?” But institutional investors can’t easily access the primary value creation — Anthropic, OpenAI, and xAI are all private. Capital is flowing to energy utilities and copper miners as roundabout bets on AI growth, missing the actual value creation entirely.

Need Inflation — The Paradox. The first four forces describe value being destroyed. This one describes value being manufactured — by the same technology, at the same time. AI doesn’t only make old satisfiers cheap. It can enlarge the need underneath them. Cybersecurity is the proof. On February 20, Claude Code Security wiped billions from vendors built on rule-based scanning — the codifiable satisfier died on schedule. Then the sector recovered, and not because the fear was wrong. AI-enabled attacks rose roughly 89% over the year that followed; autonomous hacking agents now feature in one breach in eight; a state-sponsored group hijacked Claude Code itself to run autonomous espionage against some thirty targets, the model handling 80–90% of the operation at thousands of requests per second.[19] The same capability that made the defensive product obsolete armed the attacker that made defence essential. Offence and defence are now the same technology, escalating together with no equilibrium. So the need for protection didn’t hold steady while its satisfier was automated — it inflated. CrowdStrike and Palo Alto, whose platforms sit on the growing-need side, recovered to records; legacy signature scanners, on the dying-satisfier side, did not. One sector, opposite fates, and a variable the first four forces don’t capture: not whether your value is codifiable, but whether AI grows the need you serve or merely cheapens how you serve it.

Security is the sharpest case, not the only one. The same inversion shows up wherever AI floods a domain with cheap output. As synthetic media becomes trivial to generate, the need for provenance and authenticity — content credentials, verification, proof of human origin — inflates in lockstep with the fakes. As AI agents begin to transact and decide on our behalf, the need for identity, audit trails, and trust infrastructure grows with every capability added, not despite it. And beneath all of it, AI’s appetite for compute has turned energy and grid capacity into a binding constraint the market is now pricing directly.[20] In each, AI’s abundance manufactures a scarcity beside it. That is the tell of a durable position: find the scarcity AI creates, not the abundance it captures.

These five dynamics form an interlocking system — but they don’t all run the same way. Four destroy value: platforms absorb applications because AI makes it cheap to execute documented processes; startups fail because they built businesses on codifiable workflows platforms can now replicate; incumbents lose complexity advantages because AI reads the documentation they spent decades producing. The fifth creates it: where AI inflates a need faster than it commoditises the satisfier, value flows back in. That asymmetry is the point. The market for software built on documented, codifiable work — where most startups have competed for two decades — is under accelerating pressure. The market for whatever AI makes scarce by its own abundance is expanding.

Where Value Concentrates

Not all startups are equally vulnerable. The risk — and the opportunity — depends on which of three positions they occupy.

Infrastructure — Don’t Compete Here. This is OpenAI, Anthropic, Google DeepMind, Meta AI, and xAI territory. Capital requirements are measured in billions. The global talent pool capable of frontier model training numbers in the hundreds. Open-source models (Llama, Mistral, Qwen) create alternative paths for startups unwilling to build on a single platform’s API, but commercial providers still lead on capability and enterprise support.

Tooling — Build Here at Your Own Risk. This is the position the SaaSpocalypse put under pressure. Before asking whether a platform will absorb you, ask the upstream question: is what you do fundamentally documentable and rule-based? If the answer is yes, you’re in the Tooling position regardless of how you frame it — in a documented process that AI will eventually execute more cheaply than you can. Startups that survive in Tooling survive for one reason — and it isn’t their AI capability. That’s commoditised. They survive because of proprietary data, deep workflow integration, regulatory requirements, network effects, or distribution control. Simple interface products that do nothing more than pass requests to an AI model? Six to eighteen months, at best. Tools embedded in a company’s core business systems — where permissions, data, and audit trails live — may have 2–5 years. Regulated workflows face additional friction that extends timelines further. The pace of the underlying change makes this harder to dismiss than it sounds. At GTC 2026, Jensen Huang put a number on it: computing demand increased one million times in two years, and token generation speed improved 350 times — compared to Moore’s Law’s 1.5x per year.[21] Anthropic’s Model Context Protocol is compressing what remained on the software side: what once required 18-month integration cycles to connect AI to enterprise systems now takes weeks.[22]

The burden of proof is on the startup: articulate why the platform will choose partnership over absorption, and why that choice holds for the next three to five years. If it can’t answer that question, it’s one platform update away from extinction.

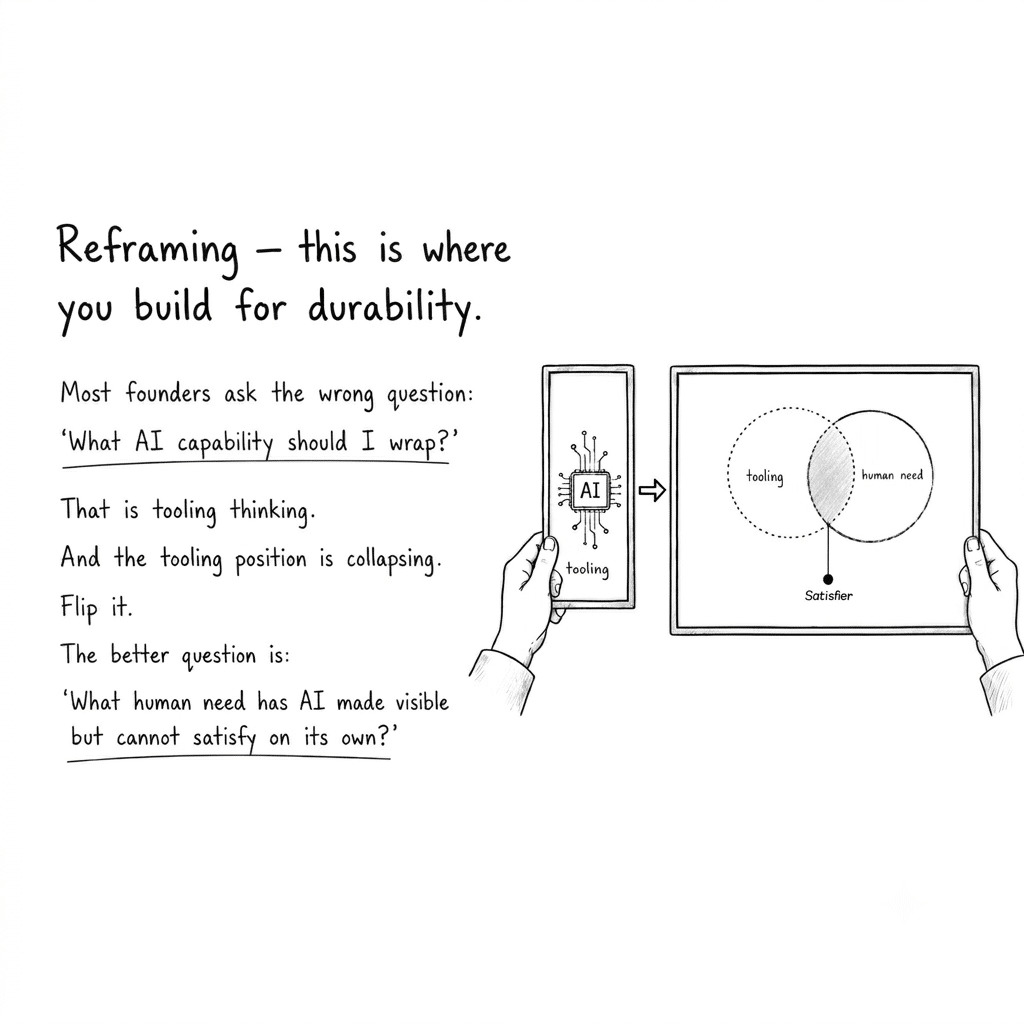

Reframing — This Is Where You Build for Durability. Most founders I speak to ask the wrong question: “What AI capability should I wrap?” That is Tooling thinking, and the Tooling position is collapsing. Flip it. The right question is: “What human need has AI made visible but cannot satisfy on its own?”

The nine fundamental human needs — subsistence, protection, affection, understanding, participation, leisure, creation, identity, freedom — haven’t changed since before industrialisation.[23] What changes, through every technological disruption, is how we satisfy them. The printing press didn’t create the need for understanding. It created a new satisfier for it. The automobile didn’t create the need for participation in a wider world. It replaced the horse as the satisfier. AI is no different. It’s making old satisfiers obsolete and demanding new ones — specifically, it’s making the codifiable satisfiers obsolete. The satisfiers that survive are those whose value is irreducibly tacit: judgment under ambiguity, contextual wisdom, cultural translation, relational trust — things that resist being written down as a procedure because they are not procedures. They have never been procedures.

But discovering a new satisfier is only half the judgment. Chegg understood the job (“pass this exam”) and built a satisfier — but AI made that satisfier free within eighteen months. The reframe was real. The durability was not. Reframing and durability aren’t sequential steps. They are two lenses that must be applied together: can you see a new satisfier that, by its nature, becomes more valuable as AI makes everything codifiable cheaper and faster? That is the entrepreneurial capability that defines the Reframing position.

Reframing: The Method Behind Durable Startups

Reframing isn’t mystical. It’s a method: identify the burden embedded in the current satisfier, then build a new satisfier that removes that burden entirely — one whose value lives in the tacit, not the documented.

Harvey AI didn’t build “better legal AI” — it reframed what legal AI should be. The old frame: AI reads documents faster, so build a research tool. Harvey’s reframe: law firms need AI integrated into their entire workflow, with liability coverage, compliance infrastructure, and institutional trust. That is not a feature. That is a different category of company entirely. Harvey reportedly grew from a $3 billion to an $8 billion confirmed valuation by December 2025. ARR reached approximately $190–195 million by year-end. There are reports of a further raise at $11 billion in early 2026.[24] Better AI models make Harvey more valuable. The scarce resource isn’t legal analysis. It’s the infrastructure between AI and institutional practice — relationships, liability, trust — and that isn’t documentable as a procedure.

Wiz reframed cloud security from reactive, periodic scanning to continuous, full-environment visibility — without requiring monitoring software installed on every server. The old frame: attach scanners, run checks on a schedule. Wiz made security ambient rather than reactive. The contrast was made explicit on February 20, when Claude Code Security wiped billions from vendors built on rule-based scanning — the exact approach Wiz had already moved away from. What collapsed was pattern-matching against a documented rulebook. What Wiz built — contextual visibility across an entire cloud environment, understanding permissions and relationships — isn’t a rulebook. It grows more necessary as cloud environments get more complex. Wiz crossed $1 billion ARR in 2025 and was acquired by Google for $32 billion — roughly 32× its projected ARR.[25]

Glean reframed enterprise search from document retrieval to institutional memory — an AI assistant that understands context, permissions, and relationships between information. It doubled revenue to $200 million ARR in nine months.[26] The moat isn’t the search. It’s the accumulated understanding of how a specific organisation’s knowledge connects. That can’t be documented anywhere. It emerges from people and decisions and history — not from a schema.

Figma reframed design from “individual desktop tool” to “collaborative browser workspace.” The reframe was so powerful Adobe attempted to acquire Figma for $20 billion; the deal was mutually terminated in December 2023.[27] Figma continued growing independently — reporting $749 million in 2024 revenue, up 48% year-on-year — and went public in 2025 at an opening market capitalisation approaching $57 billion.[28] How a specific team works, debates, and decides — that is tacit. AI amplifies it rather than replacing it.

A caution, because four winners in a row can read like a formula. Reframing is necessary, not sufficient. Chegg did reframe — it understood the real job (pass the course) and built a genuine satisfier around it — and still lost roughly 99% of its value, because the satisfier it chose was itself codifiable and AI made it free. Seeing a new frame is not the same as landing on a durable one. The path matters too: Wiz and Glean built largely net-new categories, whereas a reframer who attacks an entrenched incumbent head-on inherits that incumbent’s distribution, data, and switching costs as obstacles rather than open field. The four above are survivors; the graveyard also holds companies that reframed — toward a satisfier AI could still absorb. The test in Section 5 exists precisely to tell those two apart before the market does.

Each of these founders saw the burden embedded in the old satisfier and removed it by moving their value into territory AI can’t codify. That integrated capability — reframing the problem space and ensuring the new satisfier grows more durable as AI compresses the cost of everything documentable — remains distinctly, durably human.

Two Tests for Survival

Understanding the five forces is one thing. Knowing which side of the restructuring you’re on is another. Two tests make the diagnosis concrete.

The Durability Test is for startups — and it runs in two stages.

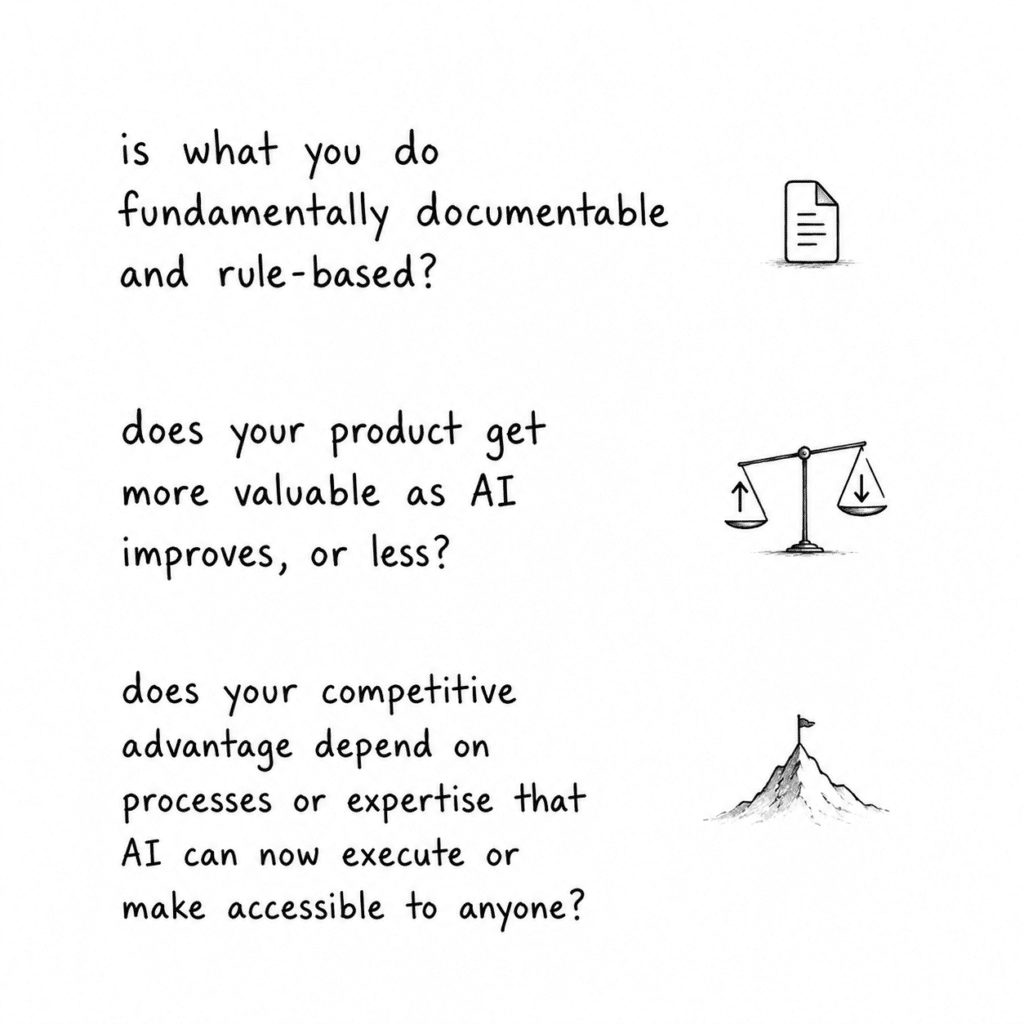

The first stage is upstream: is what you do fundamentally documentable and rule-based? If a competent practitioner could write your process down as a procedure — if this, then this — AI will execute it. And the platform will absorb it. This question comes before the product, before the market, before the funding. It determines whether you’re building in Tooling or Reframing. Most founders skip it.

The second stage is trajectory: does your product get more valuable as AI improves, or less? If a better model makes your product redundant, you’re wrapping a documented process the platform will eventually own. If a better model makes your product more necessary — because the problem it solves grows in direct proportion to AI capability — you’ve found a durable satisfier.

The two axes, drawn out. Codifiability tells you your exposure. Trajectory tells you your demand. Put them on two axes and four positions appear, not one collapsing line. Codifiable satisfier, flat or shrinking need — the Wrapper Graveyard; the platform absorbs you, and nothing replaces the demand (legacy SAST scanners, most per-seat tooling). Codifiable satisfier, inflating need — survivable only if you climb off the dying product onto the growing need fast enough; this is the security vendors who rebuilt on behavioural AI while the signature-matchers sank. Tacit satisfier, flat need — durable but not compounding; the moat is trust and it holds, but the market doesn’t grow itself (Harvey, Glean). Tacit satisfier, inflating need — the rarest, most valuable square: AI both fails to replace you and enlarges your market every time it improves. Governance of AI-mediated decisions lives here. So does AI security done right. The goal was never to escape codification alone. It is to reach the square where AI’s own progress works for you twice — by failing to copy you, and by growing what you exist to do.

When AI makes intelligence cheap, the scarce resource shifts to accountability, trust, and governance. The clearest durable position is governance infrastructure for AI-mediated decisions — audit trails, oversight of AI decisions, compliance translation. These carry liability. They require certification. They depend on regulatory relationships that platforms don’t want to own. Better AI makes these products more necessary, not less. And the window is pre-regulatory: the EU AI Act is in enforcement phase, US rulemaking is generating mandates, and the period before compliance requirements harden is the moment to build — founders who move now set the standard rather than comply with someone else’s.

The strongest case against this thesis. It deserves stating at full strength. AI may be sustaining innovation, not disruptive. Incumbents own distribution, proprietary data, switching costs, and regulatory trust — and Q1 showed them absorbing AI as a feature and growing, while the supposed disruptors stayed private and the panic reversed. On this reading nothing restructures; it consolidates, and the giants get larger. The honest answer is that this is correct — for incumbents whose moat is tacit. RELX’s legal-research corpus, IBM’s mainframe integration, a bank’s regulatory licence: AI makes these more productive, not obsolete. It is wrong for incumbents whose moat is codified — document review, migration billings, signature scanning — which is exactly where the damage landed. The bear case and this thesis are not opposites; codifiability is the line between them. It tells you which incumbents AI feeds and which it hollows. That is why the variable, not the verdict, is the thing to hold onto.

A note on limits. The Durability Test is a diagnostic lens, not a formula. The Wedbush view on Claude Code Security — that AI-native tools become additive layers rather than replacements — may prove correct in security and other regulated sectors. I think it’s right about CrowdStrike specifically. The market repricing of IBM likely overstates the near-term threat, given how much of IBM’s value sits in mainframe architecture, client relationships, and regulatory expertise that goes well beyond code translation. Enterprise buyers don’t switch at narrative timelines; sales cycles, integration costs, and risk aversion slow substitution significantly. The thesis here is simple. Codifiability determines exposure, not speed of displacement. Founders and incumbents who understand that distinction will make better decisions. The ones who either panic or dismiss the signal entirely won’t.

The Complexity Dissolution Test is for incumbents: does your competitive advantage depend on processes or expertise that AI can now execute or make accessible to anyone? The critical variable is not size — it is codification. A small firm with thoroughly documented, binary processes is as exposed as IBM. A large organisation whose value lives in undocumented practitioner judgment, relational trust, and tacit institutional knowledge? Less exposed than its scale would suggest. The question is whether your moat was built on scarcity of access to documented complexity — or on something that resists documentation entirely. IBM’s COBOL expertise, Accenture’s legacy migration billings, Bloomberg’s data aggregation advantage — each was priced on opacity that AI has made more accessible, because the opacity was, ultimately, largely documented complexity at scale. When AI reads the documentation, the advantage erodes.

The Same Line Runs Through the Org Chart

The restructuring isn’t only repricing companies. It is repricing jobs — and along the same line. On March 11, 2026, Atlassian cut roughly 1,600 roles, about 10% of its workforce. The detail that matters is where: the cuts concentrated in content, customer support, quality assurance, and project management — codifiable functions — while the company opened some 800 new roles in AI engineering, ML operations, and AI safety, and created a Chief Trust Officer.[29] Hire and fire on the same day, sorted by the same variable. The codifiable work was let go; the tacit, trust-bearing work was bought.

The pattern is broad. Block's near-4,000 cuts (Section 2) were the opening act; WiseTech then axed around 2,000. Commonwealth Bank, Australia’s largest, ran successive rounds of cuts and its CEO warned staff to expect AI-driven losses across the wider economy.[30] By early March, the tech sector alone had logged more than 45,000 cuts for the year, over 9,000 of them explicitly attributed to AI.

But the labour market shows Need Inflation too — and it shows it as a warning against reading displacement as destiny. Commonwealth Bank had earlier tied call-centre redundancies to an automated voicebot, then reversed the cuts and admitted it had mishandled them: call volumes rose, and the codifiable task (following a script) turned out to sit inside a need (a human resolving a worried customer’s problem) that had not gone away.[31] The codifiable layer automated; the human residue beneath it did not. That is the whole thesis written in jobs rather than share prices — what gets cut is the documented part, and what gets hired, or quietly rehired, is the part that resists documentation.

What This Restructuring Means

The dot-com era asked a technology-centred question: “What can the internet do?” The answer generated thousands of startups. Most were gone by 2002. The ones that survived — Amazon, Google, eBay — answered a human question instead: what do people actually need, and how does the internet deliver that differently? Technology was the enabler. Human need was the frame.

The AI era is making the same mistake faster and at larger scale. Same destination. The dominant question is “what can AI do?” — and the answer generates Tooling businesses almost automatically. When the starting point is capability, the destination is a feature. When the starting point is human need, the destination is a category. The distinction sounds simple. Almost nobody acts on it.

This is not a startup story. It is an economic restructuring — the fastest and most simultaneous compression of value across both new and established business models I’ve seen in my working life. The SaaSpocalypse put pressure on companies that built on documented, rule-following processes the platform could absorb. Established companies are discovering the same thing, from the other direction. They built their advantage on documented complexity. AI reads that documentation better than they do. Both endings were written the same way: with excessive reliance on what could be written down.

The companies that survive, whether startups or incumbents, will be those that can answer the same question from either direction: does your value deepen as AI improves, or disappear because of it? For startups, that is the Durability Test — first exposure (is this codifiable?) then demand (does AI grow the need, shrink it, or leave it flat?). For incumbents, it is the Complexity Dissolution Test — not whether you are large, but whether your advantage is documented. The test is different. The answer that matters is the same.

There is a paradox underneath all of this, and it is the message. The same force that destroys value is the one that creates it. AI does not shrink the set of things it cannot do — it expands it. Every increment of capability cheapens the codifiable and, in the same motion, raises the worth of everything that resists codification: judgment under ambiguity, trust, accountability, and — as cybersecurity now shows — protection from AI itself. Offence and defence turned out to be the same technology; the more capable it became, the more the need for the human remainder grew. “What AI cannot replace” was never a fixed list of safe harbours waiting to be eroded. It is a frontier AI keeps pushing outward as it advances, and the territory on the far side gets larger and more valuable the more powerful the technology becomes. That is the position to build on. Not where you compete with AI — where every improvement in AI makes you worth more. That is the one bet that compounds instead of eroding, and it is the only durable answer to a machine that gets better at everything documentable every month.

Notes

[1] Anthropic brings agentic plug-ins to Cowork — TechCrunch ↩︎

[2] Thomson Reuters, RELX, and Wolters Stocks Crushed After Anthropic Debuts Claude Legal Plug-In — Morningstar ↩︎

[3] Global software stocks hit by Anthropic 'wake-up call' on AI disruption — Reuters ↩︎

[4] Claude Crash Impact on Thomson Reuters + LexisNexis is Irrational — Artificial Lawyer ↩︎

[5] Anthropic Unveils 'Claude Code Security,' Sending Cyber Stocks Lower — Bloomberg ↩︎ ↩︎

[6] Anthropic's Claude Code Security launch rattles cybersecurity stocks, Wedbush sees selloff as overreaction — Yahoo Finance ↩︎

[7] IBM is the latest AI casualty. Shares tank 13% on Anthropic COBOL threat — CNBC ↩︎ ↩︎

[8] Over 70,000 AI Companies Operating Globally — HubSpot ↩︎

[9] Startup Shutdowns Jump 58% in Q1 2024 — Carta ↩︎

[10] Jasper funding, valuation & history — Contrary Research ↩︎

[11] Jasper Appoints New CEO and Cuts Internal Valuation as AI Growth Slows — Maginative ↩︎

[12] Chegg: the biggest ChatGPT / gen-AI loser — Sherwood News ↩︎

[13] Figma files for IPO nearly two years after $20 billion Adobe buyout fell through — Fortune ↩︎

[14] Jack Dorsey shrinks Block to 'intelligence-native' model, cutting 4,000 jobs — Computerworld ↩︎

[15] Jack Dorsey's 4,000 Job Cuts at Block Arouse Suspicions of AI-Washing — Bloomberg ↩︎

[16] IBM's $40B stock wipeout is built on a misconception: Translating COBOL isn't the same as modernizing it — VentureBeat ↩︎

[17] 6 Charts That Show The Big AI Funding Trends Of 2025 — Crunchbase ↩︎

[18] Introducing the Model Context Protocol — Anthropic ↩︎

[19] Manfred Max-Neef — Human Scale Development (overview) ↩︎

[20] Harvey reportedly raising at $11B valuation just months after it hit $8B — TechCrunch ↩︎

[21] Google announces agreement to acquire Wiz — Google Cloud Blog ↩︎

[22] Glean Surpasses $200M in ARR, Doubling Revenue in Nine Months — Fortune ↩︎

[23] Adobe and Figma Mutually Agree to Terminate Merger Agreement — Adobe ↩︎

[24] Figma IPO Pricing — Figma Blog ↩︎

[25] Jensen Huang GTC 2026 Keynote — NVIDIA On-Demand; coverage via SiliconANGLE ↩︎

[26] Cyber Insights 2026: Malware and Cyberattacks in the Age of AI — SecurityWeek; 2026 Cybersecurity Forecast — Cyber Defense Magazine; autonomous cyberattacks coverage — The Register ↩︎

[27] IBM Q1 2026 earnings — CNBC; RELX Q1 FY2026 — SEC; Thomson Reuters Q1 FY2026 — SEC; Anthropic & OpenAI enterprise JVs — TechCrunch; software sell-off analysis — Nasdaq ↩︎

[28] Content provenance — C2PA / Content Credentials; AI data-centre & grid demand — IEA ↩︎

[29] Atlassian follows Block's footsteps and cuts staff in the name of AI — TechCrunch; Atlassian is cutting 1,600 jobs and replacing its CTO — The Next Web ↩︎

[30] WiseTech axes 2,000 jobs, CBA cuts hundreds as AI ramps — ACS Information Age; CBA to cut 120 more jobs amid AI push — Bloomberg; Comyn warns CBA workers — Capital Brief ↩︎

[31] CBA reverses AI-linked job cuts after union pressure, admits mistake — BABL AI ↩︎

No Comments.